A HELOC quote usually shows you one number: today's payment. What it doesn't show you is the number ten years from now, when the draw period ends and the lender starts collecting principal. That second number is often the one that actually matters, and it's rarely the one people budget for.

This post walks through the actual mechanics — not marketing copy — with a worked example you can check by hand, then shows how to model your own numbers with the free HELOC Calculator.

HELOC vs Home Equity Loan vs Cash-Out Refinance

All three let you turn home equity into cash. The structural differences are what matter, not any specific rate:

- HELOC (Home Equity Line of Credit): A revolving line, like a credit card secured by your house. You draw what you need, when you need it, up to a limit. Interest accrues only on the drawn balance, not the full limit. Rate is variable by default. Sits as a second lien behind your existing mortgage.

- Home equity loan: A lump sum, disbursed once, with a fixed rate and a fixed amortization schedule from day one. You know the exact payment for the life of the loan the moment you sign. No draw flexibility — if you need more later, that's a new loan.

- Cash-out refinance: Replaces your entire first mortgage with a new, larger one, and you take the difference in cash. You end up with one loan instead of two, at whatever rate the new first mortgage carries — which resets the rate on your entire mortgage balance, not just the amount you're borrowing.

The practical filter: HELOC if you want flexible, as-needed access (a remodel with an uncertain final cost, a rolling home-improvement budget). Home equity loan if you know the exact amount you need and want payment certainty. Cash-out refi if your current mortgage rate is close to or above prevailing rates anyway, so replacing it doesn't cost you anything.

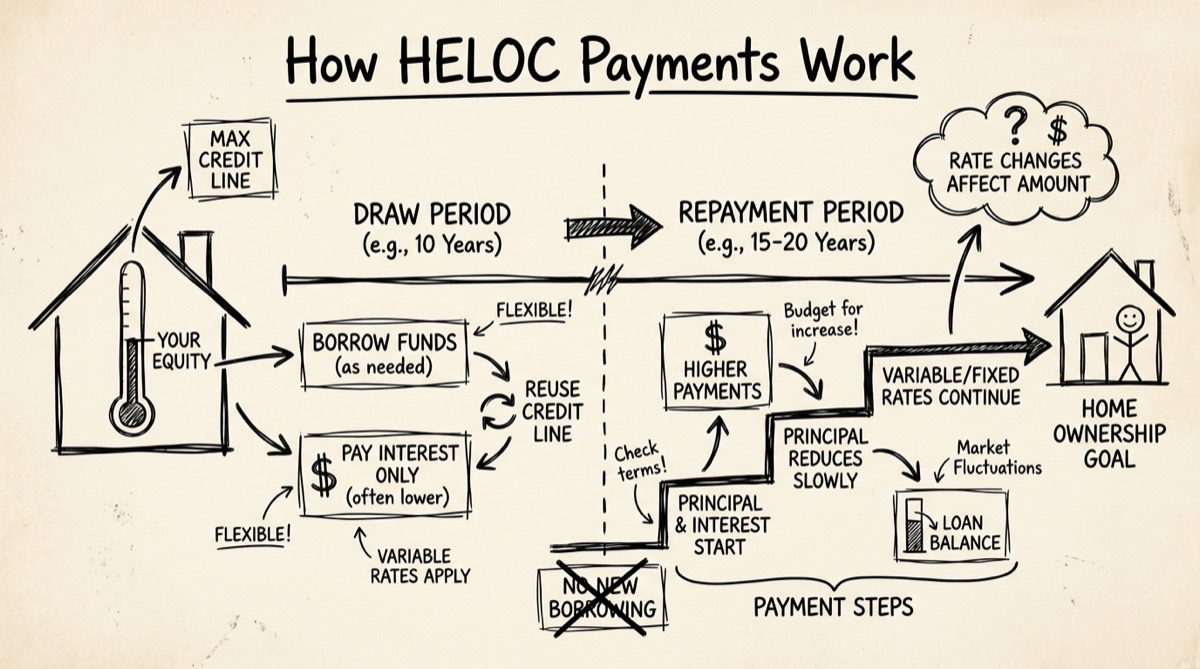

The Draw Period vs Repayment Period — Why the Payment Jumps

A HELOC has two phases, and they behave completely differently:

Draw period (commonly 10 years): You can borrow, repay, and re-borrow up to your limit. Your required payment is interest-only — calculated as balance × (APR ÷ 12). If you never pay down principal, the balance never moves, and neither does your interest-only payment (assuming a flat rate).

Repayment period (commonly 15–20 years): Draws stop. The outstanding balance is converted into a fully amortizing loan — every payment now includes both interest and principal, sized so the balance hits zero by the end of the term.

Here's the worked example, using the same math the calculator runs:

- Home value: $750,000, first mortgage: $400,000, HELOC balance: $100,000, APR: 9.0%, 10-year draw, 20-year repayment.

- Monthly rate: 9.0% ÷ 12 = 0.75%.

- Draw payment: $100,000 × 0.75% = $750/month, interest-only, for 120 months. Over the full draw period that's $90,000 in interest and the $100,000 balance is still outstanding.

- Repayment payment: amortizing $100,000 over 240 months at 0.75%/month works out to roughly $900/month — about 20% higher than the draw payment, and now principal is finally coming down.

The size of the jump is driven almost entirely by how long the repayment term is. Shorten it — a 10-year repayment on the same balance and rate instead of 20 — and the amortized payment rises to roughly $1,267/month, a 69% jump from the draw payment. Same balance, same rate, different term. This is the number people get wrong: they assume the "shock" is fixed, when it's actually a function of the repayment schedule your specific lender set, plus whatever the variable rate has done in the meantime.

How Your Credit Limit Gets Set: CLTV

Lenders don't lend against your full home value — they lend against a Combined Loan-to-Value (CLTV) ceiling:

Max credit line = (Home value × CLTV limit) − Existing mortgage balance

80–85% CLTV is the conventional range lenders use, though it's a lending convention set per-institution and per-borrower (credit score, DTI, occupancy), not a fixed rule. On a $750,000 home with an 85% CLTV cap and a $400,000 first mortgage: 750,000 × 0.85 = 637,500, minus the $400,000 already owed, leaves a $237,500 maximum line. Draw more than your CLTV allows and the lender simply won't approve it — the calculator flags this the same way, comparing your entered HELOC balance against the CLTV-derived ceiling.

The Variable-Rate Reality: Prime + Margin

Most HELOCs price off a Prime Rate + margin structure: the lender's HELOC rate floats with the published Prime Rate (which itself tracks the Fed funds rate), plus a fixed margin set at underwriting based on your credit profile and CLTV. That means:

- Your rate can change monthly, even mid-draw-period, with no action from you.

- The interest-only payment during draw moves with it — a rate increase raises your payment even though your balance hasn't changed.

- The amortized payment during repayment is recalculated against whatever the rate is at that point, not the rate you started with.

- Some lenders offer a "fixed-rate lock" option on a portion of the balance — that portion behaves like a mini home equity loan bolted onto the HELOC.

This is the structural reason to stress-test a HELOC at more than one rate, not just the one on today's quote.

How to Model Your Own HELOC

- Open the HELOC Calculator. No sign-up, nothing sent to a server — the amortization runs in your browser.

- Enter Home Value and First Mortgage Balance in the "Property & Debt" card. This drives the CLTV math.

- Set CLTV Limit and HELOC Balance. Try your lender's stated max (usually 80–85%) to see your ceiling, and your actual or planned draw amount.

- Enter APR, Draw Period, and Repayment Period in "Rate & Terms." The defaults (10-year draw, 20-year repayment) match the most common structure — change them to match your actual offer.

- Read the stat cards: draw-period payment, repayment-period payment, the exact dollar and percentage "payment shock" at the transition, your max credit line, current CLTV, and total interest split by phase.

- Scroll the chart and yearly schedule. The chart plots payment and balance across the full life of the loan so you can see the transition visually; the table below breaks out interest vs. principal per year.

- Re-run at a higher APR. Bump the rate by 2–3 points and re-check the repayment payment — this is the fastest way to see whether a rate spike would break your budget.

Honest Comparison: Other HELOC Calculators

- calculator.net's HELOC calculator — full amortization table, no email required, but it's a generic finance-calculator template with ad placements around the results.

- Bank of America / mortgage.com HELOC calculators — polished, but built to route you into an application funnel; several fields nudge you toward "get a rate" forms that capture contact info before showing real numbers.

- Point's interest-only HELOC calculator — good for the draw-period math specifically, less built out for the repayment-period transition.

- CNBC Select's HELOC guide — a solid written explainer with one static worked example, but it's an article, not an interactive tool — you can't plug in your own numbers.

None of them are wrong, exactly — the math is the same math everywhere. The differences are about who's collecting your contact information and how much of the repayment-period picture they actually show you. If you just want to enter numbers and see the full draw-to-repayment schedule without a lead form in the way, that's what the orangebot version is built for — it's also useful precisely because it stays out of your inbox afterward.

FAQ

What's the real difference between a HELOC and a home equity loan?

A HELOC is revolving — draw, repay, redraw, up to a limit, with a variable rate. A home equity loan is a one-time lump sum with a fixed rate and a fixed payment set at closing. If you need payment certainty, the home equity loan removes the guesswork; if you need flexible access over time, the HELOC does.

Why does my HELOC payment jump so much after the draw period?

Because you switch from interest-only to fully amortizing. During draw you're only covering the interest that accrued; during repayment you're paying that interest plus enough principal to zero out the balance by the end of the term. The size of the jump depends heavily on how long your repayment period is — a shorter repayment term forces a bigger monthly increase for the same balance.

How much HELOC can I actually qualify for?

Lenders cap it via Combined Loan-to-Value: (home value × CLTV limit) − existing mortgage balance. 80–85% CLTV is the common convention, but your actual limit also depends on credit score, income, and the specific lender's policy — treat CLTV math as an estimate, not a guaranteed approval.

Is a HELOC rate fixed or variable?

Almost always variable, priced as Prime Rate plus a margin set at underwriting. Both your draw-period interest-only payment and your repayment-period amortized payment can change as the underlying rate moves — a HELOC does not lock in a rate the way a home equity loan does, unless your lender offers a specific fixed-rate-conversion option on part of the balance.

Can I pay down principal during the draw period even though it's not required?

Yes, and it's usually a good idea if you can. Any extra payment during draw reduces the balance the interest-only payment is calculated against, and it reduces the balance that gets amortized once repayment starts — directly shrinking the size of the payment jump.

Is my financial information safe when I use an online HELOC calculator?

Depends on the tool. Many lender calculators are wired to capture your contact details before showing full results. The HELOC Calculator on orangebot runs the amortization entirely client-side in JavaScript — nothing you enter is sent to a server, and there's no form to submit.

For the mechanics behind the mortgage sitting underneath your HELOC, see how mortgage payments are calculated. If you're thinking about a HELOC as leverage rather than just a renovation fund, leverage, position size, and liquidation covers the same math from the borrowing-against-an-asset angle. For the rest of orangebot's free, browser-only finance and utility tools, see /tools.